On speculative bets and cryptocurrencies.

A recent post caught my attention by @HsakaTrades, which was further quote tweeted by @ZhuSu. Both of them are rather large and important folks in the weird realm known as Crypto Twitter.

Crypto Twitter is perhaps more important, dollar for dollar, than Financial Twitter itself (even if many on FinTwit would like to view it as some weird benign tumor that fissioned off of FinTwit), because rather unlikely FinTwit Crypto Twitter (or CT, as many call it) actually makes money, Both in the way that the largest, most notable accounts on CT tend to be actual crypto whales (such as Zhu Su, who heads Three Arrow Capital), and because the crypto economy is profoundly impacted by sentiment, which can be gauged by looking at Twitter quite well (more on this at a later post probably).

To give a brief primer on cryptocurrencies, the universe roughly looks like:

Similarly, despite the massive recent press it receives, the current market capitalization of the entire lit cryptocurrency universe is around $2.2 trillion, making it comparable in notional value to about one Microsoft Corporation (aka if the entire crypto-economy was one company, it would not even be the largest public company on Earth currently).

For most of crypto’s history, Bitcoin was the flag-bearer asset of the technology, being created in January 2009 and disseminated by a small group of dedicated hacktivists via SourceForge. This dominance dropped permanently and profoundly by the launch of the Ethereum network in 2015, nearly six years after the launch of Bitcoin itself. Unlike Bitcoin, Ethereum was formed by a dedicated and funded group of engineers, where a substantial portion of the network’s coin, Ether (yes, the coin is called Ether and the network is Ethereum, they are not the same) was pre-mined for funders and the founding team.

That said, there’s a rather large vein of thought in the cryptocurrency community about the idea of “lindyness”, or that the value of all assets increases as a function of time-to-live. This trivially makes sense in the most base case for something like a country’s fiat currency — a newly formed regime issuing paper currency (e.g. the Continental Congress after the Revolutionary War) has minimal authority and creditworthiness, while 250 years later the U.S. Dollar is considered the reserve currency of reserve currencies. However, it’s hardly a fixed rule economically, but it becomes important in understanding cryptocurrencies.

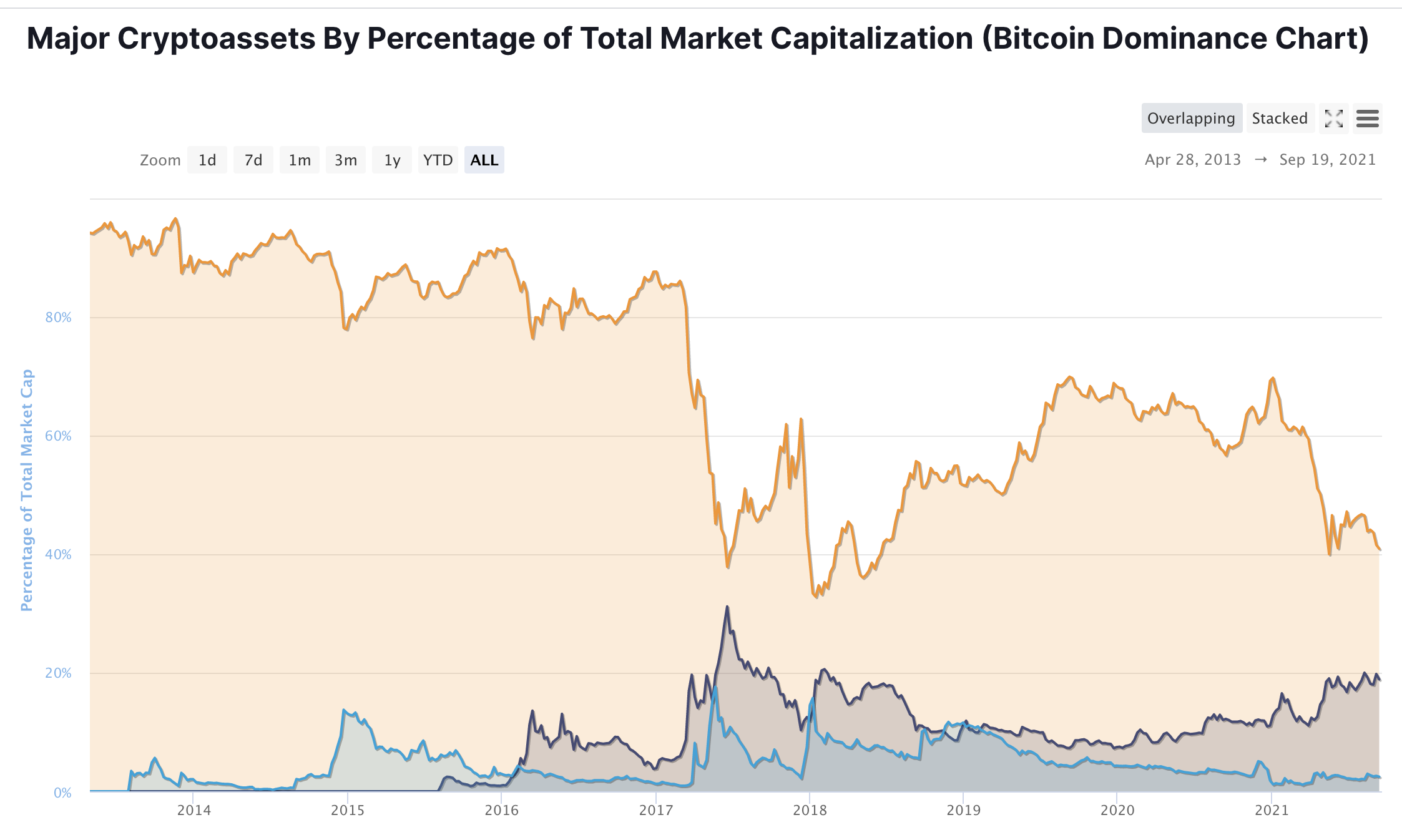

Although I could rant philosophically about Bitcoin’s place in the crypto universe, the important takeaway here is the cementation of the idea of Bitcoin dominance — for many reasons (branding/mindshare, lindyness, liquidity, decentralized creation), many view the health of Bitcoin and its little-but-different brother Ethereum as deciding the overall health of the cryptocurrency universe. With recent pushes to portray cryptocurrency as a multi-chain asset class (or, in English, a focus on having separate, exclusive blockchain networks (“L1s”)), it’s still undeniable that even to the present the dominance of Bitcoin and Ethereum is unparalleled. Together, even in the midst of profound altcoin radiation, DeFi, and NFT mania, both coins represent nearly 61% of the cryptocurrency market.

But this isn’t what I want to talk about either. A much more interesting and perhaps insidious phenomenon is the idea of “altcoin season”, which historically tends to occur towards the end of cryptocurrency bull runs.

Harkening back to my liquidity series, there is a lot of fundamental variance in the cryptocurrency markets. In fact, unlike a “hard” asset (and I’m using the word hard liberally here, including things like equities for example), the value distribution of a cryptocurrency’s value for sure overlaps. on the low end and perhaps nearly infinity on the high end. Even with implied network valuations, one could confabulate future scenarios where we all use GalaxyCoin and the entire wealth of the universe is locked under SHA-1024 (I assume this version should be resistant to Shor’s algorithm, god help us).

Largely due to fundamental variance and the massive amounts of financial leverage pulsing through the cryptocurrency ecosystem (mostly due to lack of regulation or fears of systemic contagion, unlike the highly regulated equities markets), cryptocurrency (Bitcoin for example) has a high tendency to undergo bubble periods, sparked usually by some macroeconomic event (or, if you drink the Koolaid, potentially due to miner halving rewards). We can observe this quite cleanly in the Long View of Bitcoin history (aka its chart against USD back to 2010 or so):

This isn’t an argument on if Bitcoin is heading to zero. That said, one can note cleanly on the logarithm chart alone that Bitcoin tends to undergo bubbly spurts every few years, where its value dramatically increases only to fall precipitously soon after. Notably, this bubble dynamic has a significant positive drift — rarely, if ever, have post-bubble prices ever returned to pre-bubble prices (or in English, after each bubble pop the floor seems to rise).

During these bubble periods, cryptocurrency becomes the zeitgeist, and receives substantial amounts of mainstream coverage and adoption. This was less of the case in earlier years (when Bitcoin/crypto was still a niche asset), but has become more and more prominent as every subsequent bubble cycle has progressed.

According to Statista, in 2019 75% of US respondents were aware of Bitcoin in 2019, at the troughs of the last bear cycle. One can imagine the number is nearly 100% now.

However, the most stylized fact of Bitcoin bubble periods tends to be the rise of alternative coins (altcoins). Many argue that Ether (Ethereum) is itself an altcoin to Bitcoin, but its massive rise and sprawling ecosystem may beg to differ.

But, without splitting hairs or angering too many camped maxis, we can see cleanly in the CoinMarketCap chart the effect of cryptocurrency bubbles on Bitcoin dominance.

We can note from the 2017 and 2020 trends the most interesting phenomenon — Bitcoin dominance, at the macro scale, seems inversely correlated to Bitcoin price. This isn’t a week-by-week phenomenon, but becomes apparent at the yearly or longer view. Or more succinctly, the rise of altcoins seems predicated on Bitcoin’s bubbly ascent. During quiescent periods (e.g. mid 2018 to early 2020) Bitcoin dominance increased gradually over time, largely at the expense of non-Ether coins.

A second, more unfortunate stylized fact about cryptocurrency is the idea of correlations. Much like the comovement of equities in indices, on the way up there is some radiation and separation of cryptocurrency prices. On the way down — much less so.

At the start of new or niche altcoin/cryptocurrency projects, one can expect substantially more price appreciation than much later in the game, on a more established asset like Bitcoin or Ether. As it matures, this tends to level out, but owing to the network size, mindshare, and “lindyness”, in general guessing correctly on an altcoin lends to higher returns than on Bitcoin itself.

However, this is well described by normal corporate finance — undeniably, one assumes substantially more risk. An altcoin is not simply a bet on the project’s success (i.e. I may be super bullish on dog food delivery using GalaxyCoin), but on the cryptocurrency universe at large. Bitcoin in essence still represents the “purest play” on cryptocurrency, and can largely be seen in the context of cryptocurrency as having minimal other idiosyncratic risk (important to underline this here — cryptocurrency itself is massively risky, but going long Bitcoin itself does not add more risk).

This is also well described as a type of synthetic, non-recourse leverage. How does this work akin to leverage (non-recourse)? The dagger of leverage normally cuts both ways — when I assume a levered bet (let’s say to be spicy a 20x long position on Bitcoin), I am in theory assuming responsibility not only for a full loss of my initial position, but in some cases can end up owing far greater sums if I get profoundly unlucky. Due to the unregulated and trustless nature of cryptocurrency, most highly levered positions become pseudo-non-recourse via exchange-triggered liquidations, which lead to fun effects like liquidation cascades.

When I buy into a new altcoin project, I can decompose the position into two return factors — the cryptocurrency factor (which we can, old-school, peg to Bitcoin’s returns over a given period) and the idiosyncratic risk of the altcoin itself.

In periods where Bitcoin is trending unidirectionally (up only, obviously), I can replicate the returns of an altcoin via a leveraged Bitcoin position instead, replicating the idiosyncratic returns of the altcoin. But, unlike the altcoin, the leveraged position on Bitcoin has several benefits.

Bitcoin, owing to its dominance and decentralized origin, has a few favorable factors over SomeRandomAltcoin for an identical return stream:

1) Liquidity - While order flow in cryptocurrencies tends to be highly correlated as is (and realized volatility is very sticky), it’s very rare to encounter a truly illiquid Bitcoin (or Ether) market. This tends to occur only in special periods of highly imbalanced order flow, like liquidation cascades. Conversely, a new altcoin project will have highly concentrated initial liquidity, which has a strong tendency to become more illiquid over time.

2) Longevity - This is the lindy thesis of Bitcoin in general. Despite all its problems, Bitcoin has lasted for over 10 years now, and enjoys the largest public mindshare, regulatory support, and institutional investment. Conversely, altcoin radiation tends to occur quickly, largely driven by retail fervor, and shows especially dramatic sensitivity to binary catalysts/macro events.

3) Accessibility - Many altcoin projects tend to be fairly inaccessible, which contributes to their illiquidity. This is both a marketing and a technical issue. Unlike Bitcoin (and more recently, Ether), which enjoy access from multiple physical and virtual venues, many newer projects require complicated bridging or technical steps which profoundly limit accessibility. This decreases network adoption, and increases sensitivity of price and liquidity to events and zeitgeist chanfges.

4) Security - As noted above, in a trustless and anonymity-driven environment, many altcoin projects suffer from unclear developer and “whale” intentions. While Bitcoin certainly is a top-heavy asset in terms of ownership, the origin and disappearance of its pseudonymous creator Satoshi Nakamoto makes it profoundly unlikely to be rugpulled.

So, it’s fairly undeniable that the returns profile of an altcoin can be mimicked in bubbly periods by a levered position on Bitcoin or Ether. This tends to have certain attractive qualities over the altcoin itself. So why does altcoin season happen?

Volume.

While this isn’t a hard and fast rule, altcoin season tends to occur at the tail end of the Bitcoin bubble epoch. Certain altcoins show substantial gains pre- and during the bubble itself, but the notable public consciousness and profound maniacal gains tend to occur in the later stages. To see this, we can look no further than cryptocurrency’s prodigal son, Dogecoin:

Dogecoin has always been the red-headed stepbrother of the cryptocurrency universe, because although it has nearly all the same properties of Bitcoin and other cryptocurrencies — it’s clearly also a joke. Very few people take Dogecoin seriously, and this tends to present an uncomfortable dark mirror to the Bitcoin and Ether maxis of the world (I’m sure someone will list the technological differences in the comments, and although I’m aware of them — it also hardly matters here).

Dogecoin I’ve previously noted acts akin to a “crypto-VIX”, tending to rally towards the end of maniacal bull periods. This is consistent with wider adoption, and buoyed by the low unit price and thin order book (even more so than Bitcoin, DOGE is almost exclusively held by whales who are happy for any and all exit liquidity).

We can observe quite clearly that over the past year, Dogecoin rallied almost 10,000%. Bitcoin, conversely, only went up a paultry 350% in the same timeframe.

So, despite its self-effacing nature, Dogecoin net net was the “better’ investment. But, more notably, Dogecoin is also down nearly 70% from its intra-2021 high at present, compared to Bitcoin’s comparatively minor 20-30% drop. This is highly consistent with the idea of synthetic leverage — while Dogecoin rallied harder, it also dropped harder than the cryptocurrency factor (Bitcoin). It’s still notable that even from a synthetic leverage perspective, Dogecoin wins out (it returned much higher returns compared to the amount it dropped). This is not true for most altcoins, however.

The beauty of altcoins tends to be in the amount of volume needed to push price. Bitcoin, like most bubbly assets, goes through periods of strong, multi-day trending, coupled with quiescent, mean-reversionary periods. The quiet periods tend to also demonstrate petering volume; like most speculative assets, cryptocurrencies tend to show substantial volume on the way up, with diminishing volume in quiet, bearish periods (the notable exception is during crashes, of course). However, during those same periods, owing to the prevalence of institutional-grade market makers and prop traders, the Bitcoin order book remains thick. It is much more difficult to move Bitcoin price over any timeframe than an altcoin.

Mean reversion, of course, is the enemy of a leveraged trader. Even given the non-recourse-like structure of most crypto exchange-based leverage (aka liquidations), it becomes profoundly more difficult to hold a leveraged position on a mean reverting asset, especially at high leverage (which tends to, as we recently observed again, be a strong driver of crypto-momentum).

So, what does a degenerate do when his drug of choice (leverage) meets a weak price trend and bullish volume starts to peter out?

He moves to altcoins.

Altcoins represent synthetic leverage to a degree against cryptocurrency itself, with the significant benefit that the order book is thin and price can move quite easily. Properly structured bets coupled with social media outreach can make 10x’ing your money on altcoin much simpler than the equivalent levered Bitcoin bet. However, when Bitcoin itself is trending — they present a substantially worse proposition than the equivalent levered Bitcoin position.

As the bull market stars to peter out, the volume associated with bubble frenzies starts to dive as well. This makes it substantially more difficult to move Bitcoin price up in a way that suits leveraged bets, and leads migration into altcoins and other “riskier” cryptocurrency bets.

Is this pattern going to last forever? It’s unclear. But enjoy it while it lasts, and stay safe.

Best,

Lily

The greatest trick the devil ever pulled was convincing BTC hodlers that miners would continue to secure the network past the point where there are not enough transaction fees contained in a block, plus the diminishing block reward, to make mining economic.

Great post, just missed the rebuttal to Haka :p